- Bank /

- NPL: Curse for sustainable growth

SAM

Published:2018-04-12 18:40:59 BdST

NPL: Curse for sustainable growth

FT ONLINE

Now that Bangladesh has met all the criteria for graduating into a developing country all efforts should be made to strengthen the banking sector.

The requirements and challenges of many to a developing country must not be ignored and the best way to do this is TO strength the capital and liquidity ratio of the banks, according to the editorial of the current News Bulletin (Jan-Mar’ 2018) of International Chamber of Commerce-Bangladesh (ICCB) released on Wednesday.

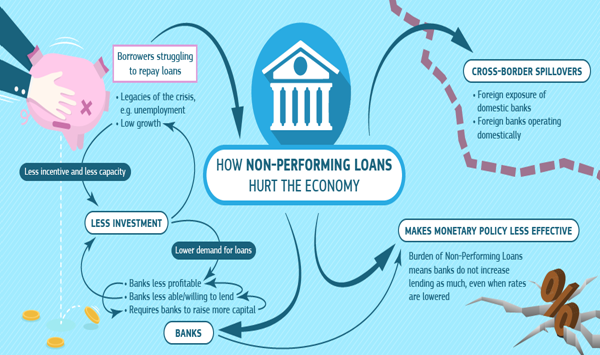

Non-Performing Loans (NPL) is one of the issues that is impacting capital adequacy of the industry, especially the eight state-owned commercial and specialised banks. For decades, state-owned banks have been the prime leader to the large corporate borrowers particularly in the industrial sector of the economy.

The prerequisite for the economic development of a country is smooth and efficient flow of saving-investment process. Bangladesh, being a developing country and with an underdeveloped capital market, mainly depends on the intermediary role of commercial banks for mobilising internal saving and providing capital to the investor. Thus, it matters how well our financial sector is functioning.

In Bangladesh six state-owned commercial banks account for about a quarter of total banking sector assets. They are supplemented by two state-owned specialised development banks, 40 private commercial banks and nine foreign banks.

Capital adequacy is the primary indicator of the banks’ financial fitness and stability. After successful implementation of Basel II guideline in regards to the adequacy of capital, Bangladesh Bank is now in the process of implementing Basel III guidelines which is an international regulatory framework for banks.

According to a Bangladesh Bank study five years (during CY2012 to CY 2016) average ratio of gross NPLs to total loans were about 27.1 per cent, whereas, it was 4.9 per cent for PCBs, 6.5 per cent for FCBs & 22.56 per cent for SCBs. The per centage of classified loan to total outstanding stood at 10.1 per cent in June 2016. The per centage was highest for the SBs 26.1 per cent, for the PCBs 5.4 per cent, for the SCBs 25.7 per cent and for the FCBs 8.3 per cent.

Until September 2017, total banking sector loan amounted to Tk 7,527.30 billion, of which Tk 803.07 billion or 10.67 per cent was bad debt. And if restructured or rescheduled loans were included, NPL in the banking sector goes up to 17 per cent of total outstanding loans.

By the end of September, the total bad debt of SCBs stood at Tk385.17 billion against the disbursed loans of Tk1,316.89 billion (29.25 per cent of disbursed loan); total bad debt of specialised Bangladesh Krishi Bank and Rajshahi Krishi Unnayan Bank stood at Tk 55.18 billion against the disbursed loans of Tk 231.93 billion (23.79 per cent of disbursed loan); PCBs had default loans of Tk 339.73 billion against the disbursed loans of Tk5,687.32 billion (5.97 per cent of disbursed loan) and FCBs had bad debt of Tk 22.98 billion against the disbursed loans of Tk291.16 billion (7.89 per cent of disbursed loan).

Naturally, these high NPLs have affected the profitability and the overall capital to risk weighted assets ratio (CRAR), a key measure of bank strength and stability. According to The Economist's Intelligence Unit, The CRAR at private banks was 12.2 per cent, while that at the nine foreign banks was a healthy 23.9 per cent , the six state-owned commercial banks was only 5.9 per cent and that of the two specialised state-owned banks was an astonishing -35.23 per cent.

Further bad loans are routinely restructured to permit further lending to the same borrowers. According to a study by the Bangladesh Institute of Bank Management (BIBM) an average banks rescheduled bad loans of Tk 109.1bn annually during 2010–14.

According to a meeting of the parliamentary standing committee on finance ministry at the Jatiya Sangsad Bhaban on February 28 the amount of defaulted loans of top 25 defaulters stood at Tk 96.96 billion as of September last year. The central bank submitted the list at parliamentary standing committee suggested forming a joint committee comprising BB and finance ministry officials.

In contrast, to recapitalise banks over the past few years the government has provided large amounts to the sector. In the budget 2017/18 the government has earmarked Tk20bn to recapitalise state-owned banks. The decision to provide funding has been criticized by the experts. As despite the regular infusion of budget funds, state-run banks have not improved their NPL positions.

Until now, only limited action has been taken to penalise defaulters, improve risk management and strengthen bank management. To tackle the sector's deep-rooted problems of corruption and poor risk practices further efforts needed.

Unauthorized use or reproduction of The Finance Today content for commercial purposes is strictly prohibited.